DeFi – where the money comes from and who’s paying for it

Another shot at explaining how the DeFi ecosystem actually works.

Save this post – you might want to revisit it later, mostly for understanding where does the yield come from.

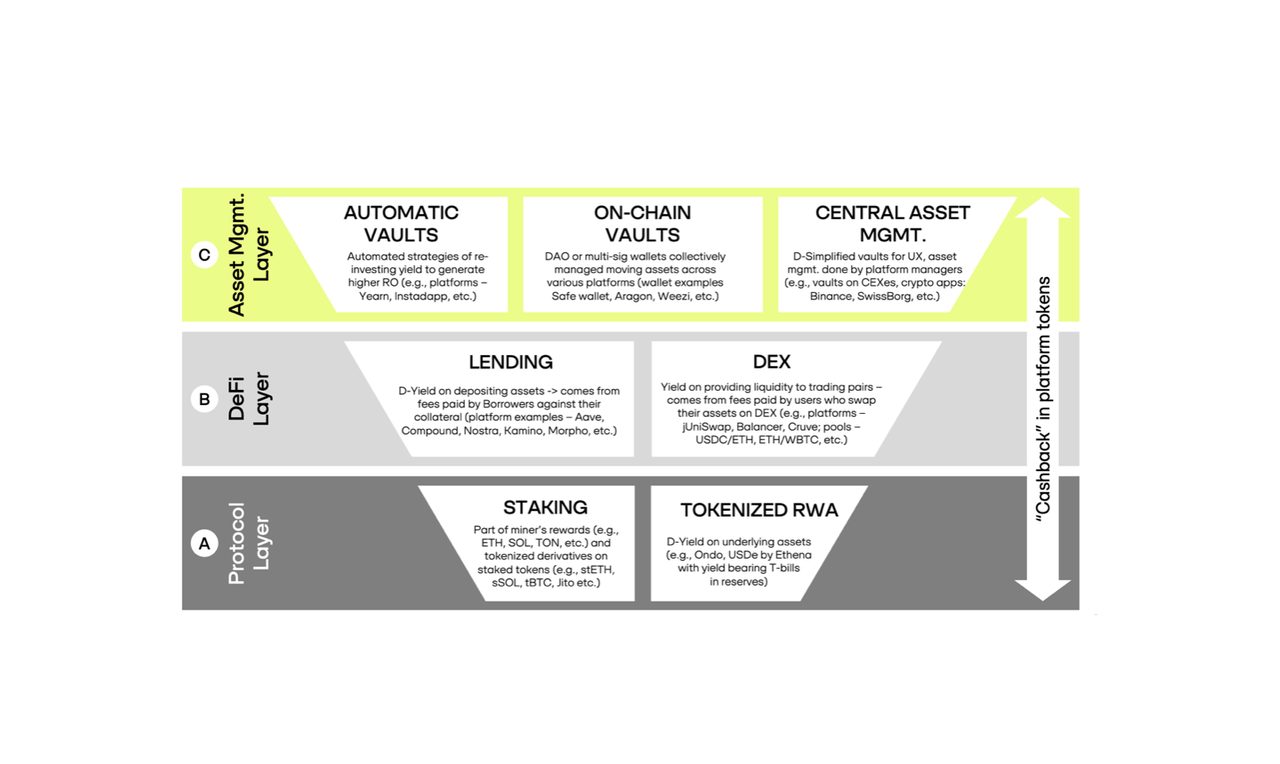

The easiest way to think about DeFi is as a three-layer system, where each layer sits on the shoulders of the layer below.

A – The Protocol Layer

This is the foundation, where the core infrastructure generates revenue.

- Staking – With most blockchains shifting to a proof-of-stake consensus model, regular users like us now have the opportunity to tap into what used to be “miner revenue.” In simple terms, those who run blockchain networks by maintaining servers get rewarded in the network’s native tokens (ETH, SOL, TON, Jito etc.). The more assets they lock up, the bigger the rewards. So, to maximize their earnings, these validators invite everyday users to stake their tokens through them. In return, they share a portion of their staking rewards from such protocols with us.

- Tokenization of Real-World Assets (RWA) – Imagine any traditional asset that generates revenue. Now picture a legal entity securing ownership of that asset and issuing a token backed by it, distributing earnings to token holders. The most popular example in crypto today? Stablecoins backed by government treasury bonds. One of the hottest cases right now is Ethena’s USDe token, which follows this model. Ondo is another example. And this is just the beginning – soon, we’ll see tokenized versions of everything from real estate to credit instruments.

Tokenization of Real-World Assets is just the beginning – soon, we’ll see tokenized versions of everything from real estate to credit instruments.

B – The DeFi Layer

This is where financial applications come in.

- Lending Protocols – Think of it as automating a standard collateralized loan or a broker’s repo transaction. Users deposit assets they don’t want to sell (BTC, ETH, SOL, etc.) as collateral and borrow stablecoins (USDT, USDC) or other tokens against them. Whether it’s for a coffee run or high-leverage trading, borrowers pay an interest fee. That interest is partially distributed to those who provided their USDT/USDC as deposits. Example of Platforms like Aave, Compound, Nostra, Kamino and Morpho make this possible.

- Decentralized Exchanges (DEXs) – These automate crypto asset swaps. Similar to airport currency exchange kiosks where users swap dollars to the local currency while paying a commission, DEXes charge trading fees. These fees go to liquidity providers who supply the exchange with cash. Unlike airport exchanges, which won’t let you participate in their earnings, platforms like UniSwap, Balancer, and Curve allow users to provide liquidity (e.g., ETH/USDC, WBTC/USDT,..) and earn a share of trading fees.

C – Asset Management Layer

At this level, no new paying clients appear. Instead, increased returns are generated through two approaches:

i) Reinvesting accumulated income back into the principal investment (compounding interest).

ii) Moving assets between protocols to find better yields.

Crypto asset management can be grouped into three methods:

- Automatic Vaults – Primarily used for reinvesting yield, automating leverage, etc. Examples: Yearn, Instadapp.

- On-Chain Vaults – DAOs or multi-signature wallets managed by a group through voting and transaction approvals. Funds are moved across platforms to optimize yields. Examples: Safe, Bitpay, Aragon, Weezi, xDAO; management examples: Berezka DAO, DeFi Pulse, Mev Capital.

- Centralized Asset Management – Centralized solutions provided by exchanges (Binance, ByBit) or wallets (SwissBorg) offering investment products with simple interfaces (1-2 clicks). These platforms manage user funds and earnings behind closed doors, with no on-chain transparency.

D – A Side View

In addition to the four revenue models at A and B and the three yield-boosting methods at C, there’s also a D-layer: platforms rewarding users with cashback in the form of their own tokens as an incentive for engagement.

DeFi Asset Management boils down to two things: 1. compounding interest by reinvesting income, and 2. optimizing yields by shifting assets between protocols.

Now, let’s try to assemble the DeFi puzzle!

Let’s imagine that every platform we use rewards us with cashback in the form of their own tokens. What would that look like?

- We start at the protocol level. First, we wrap our ETH on Lido to receive stETH, and on Ethena, we swap USDT for USDe. In both cases, we begin earning yield on these wrapped assets. Lido could rewards us with its native token, LDO, while also providing staking rewards of around 3% on ETH. Meanwhile, Ethena offers a return of around 5% per year from U.S. Treasury bills and may distribute additional ENA tokens to users.

- From here, we move up to the DeFi level, where we deposit our stETH and USDe into lending platforms like Morpho. This allows us to earn interest on our deposits, and at the same time, Morpho may reward us with its own tokens for using the platform.

- Finally, we take things a step further by leveraging asset management solutions. We use Instadapp to increase our yield through automated leverage and reinvestment of earned interest. This not only enhances our overall returns but also, hypothetically, earns us additional INST tokens for interacting with the platform.

As a result, for the investment in the form of ETH + USDT tokens we receive:

⁃ Income from staking + tokenization

⁃ Income from the deposit on Morpho

⁃ Increased income due to automated leverage on Instadapp

⁃ Additional tokens of all used platforms – LDO, ENA, Morph, INST (hypothetical example)

Keeping track of all these strategies manually can be overwhelming. That’s why asset management solutions are rapidly emerging, simplifying the user experience and making these strategies more accessible. Stay tuned for more yield and automation ideas in DeFi.

Oleg Ivanov, COO & Co-Founder SecondLane